Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

30 March, 2020

9 Min Read

Part of: GS Prelims and GS-III- Economics

Recently, the State government of Kerala has sought flexibility under the Fiscal Responsibility and Budget Management (FRBM) Act.

Reasons for Seeking Flexibility

|

FRBM Act

Relaxation under the FRBM Act

Instances of the FRBM Norms been Relaxed in the Past

|

NK Singh FRBM review committee

The FRBM Review Committee headed by former Revenue Secretary, NK Singh was appointed by the government to review the implementation of FRBM. In its report submitted in January 2017, titled, ‘The Committee in its Responsible Growth: A Debt and Fiscal Framework for 21st Century India’, the Committee suggested that a rule-based fiscal policy by limiting government debt, fiscal deficit and revenue deficits to certain targets is good for fiscal consolidation in India.

Why a rethinking on FRBM was needed?

After nearly twelve years into running of the FRBM (2003) legislation, there was a big debate on whether India has to continue with a fiscal deficit target or not. One group argued that in a developing country, the government has to make lot of expenditure and an upper ceiling will reduce government involvement. The opposite group countered that loosening the target will lead to excess expenditure, government debt, inflation and several other macroeconomic problems besides creating intergenerational inequality. The responsibility of the NK Singh Committee thus was to suggest a way out. Specifically, the Committee has to make suggestions on a commonly raised idea of a fiscal deficit range than a fixed target (like 3% of GDP). Similarly, the committee should suggest changes required in FRBM in the context of rising global uncertainties.

The general perspective of the FRBM Review Committee

Before going into the point-by-point presentation of the NK Singh Committee’s suggestions, it is important to look at the overall perspective adopted by it about the borrowing run (fiscal deficit) government budget in the Indian context.

The FRBM Review Committee’s philosophy is visible in its report throughout and is that in a country like India, where budgets are framed by accommodating populist pressures, activist or discretionary fiscal policy with a high fiscal deficit has limitations.

“The maxim that “you cannot spend your way to prosperity” is now widely accepted. Fiscal policies must therefore be embedded in caution than exuberance. In restraint than profligacy.” The Committee cited evidence that in the recent past, the economy faced troubles whenever the government made high expenditures by shooting over the FRBM targets.

At the same time, when some crisis like 2007-08 appears, fiscal policy should have some flexibility. Here, the Committee suggested a carefully crafted escape clause allowing higher fiscal deficit. This escape clause is ‘rule based’ (smart rules) and not ‘discretionary’. Following are the main recommendations of the NK Singh Committee.

1. Public debt to GDP ratio should be considered as a medium-term anchor for fiscal policy in India. The combined debt-to-GDP ratio of the centre and states should be brought down to 60 per cent by 2023 (comprising of 40 per cent for the Centre and 20% for states) as against the existing 49.4 per cent, and 21per cent respectively.

2. Fiscal deficit as the operating target: The Committee advocated fiscal deficit as the operating target to bring down public debt. For fiscal consolidation, the centre should reduce its fiscal deficit from the current 3.5% (2017) to 2.5% by 2023.

Justifying the target of 2.5% to be realized in the next six years, the Committee observed that debt sustainability analysis (DSA) conducted for the central government suggests such a target (for fiscal deficit) will help to achieve the public debt target of 40% for the centre by 2023.

3. Revenue deficit target

The Committee also recommends that the central government should reduce its revenue deficit steadily by 0.25 percentage (of GDP) points each year, to reach 0.8% by 2023, from a projected value of 2.3% in 2017.

The Committee advised the government to follow the golden rule here ie., not to finance the government’s day-to-day expenditure through borrowings. Revenue deficit implies financing of government’s day to day activities from borrowings.

Table: Fiscal roadmap for 2023 and the targets for the Centre (figures are as a percent of GDP) FD is fiscal deficit and RD is revenue deficit.

Year Debt/GDP FD RD

2017 49.4 3.5 2.3

2023 38.7 2.5 0.80

Source: NK Singh Committee Report

4. Formation of Fiscal Council to advise the government.

The Committee advocated the formation of institutions to ensure fiscal prudence in accordance with the FRBM spirit. It recommended setting up an independent Fiscal Council. The Council will provide several advisory functions. It will forecast key macro variables like real and nominal GDP growth, tax buoyancy, and commodity prices. Similarly, it will do a monitoring role, besides advising about the use of escape clauses and also specifying a path of return.

5. Escape Clause to accommodate counter cyclical issues:

The NK Singh Committee points out that there are disadvantages with set fiscal deficit target if some economic instabilities like an external crisis affects the Indian economy. For example, the government has to spend more during the time of a recession and hence it need not restrict its borrowing to keep the fiscal deficit target. Hence, the committee advocates countercyclical covers in fiscal policy while following the FRBM.

Here, the committee recommends fiscal flexibilities to go above or below the fiscal deficit targets in the form of ‘escape clauses. The Committee set 0.5% as an escape clause for the fiscal deficit target.

What is an escape clause?

The flexibility to adjust to cyclical fluctuations (boom/recession) is incorporated under the “escape clause” (in the case of recession) where temporary and moderate deviations can be made from the baseline fiscal path. This can be permitted under exceptional circumstances and in reaction to external shocks. To ensure that these “escape” clauses are not misused, the Committee suggests several specific guidelines. The escape clause can be used only during the time of following essential circumstances:

• Over-riding consideration of national security, acts of war, calamities of national proportion and collapse of agriculture severely affecting farm output and incomes.

• Far-reaching structural reforms in the economy with unanticipated fiscal implications.

• Sharp decline in real output growth of at least 3 percentage points below the average for the previous four quarters.

Deviation from the stipulated fiscal deficit target shall not exceed 0.5 percentage points in a year.

The Escape Clauses can be invoked:

(a) by the Government after formal consultations and advice of the Fiscal Council.

(b) with a clear commitment to return to the original fiscal target in the coming fiscal year.

6. Buoyancy: What the government has to do with fiscal deficit target when higher economic growth occurs?

The Committee also advocates that that the policy responses to sharp changes in output growth should be symmetric (to that of the escape clause). This implies that during higher economic growth, fiscal deficit should be reduced accordingly. (Here, in the case of growth fall, fiscal deficit target can be raised using the escape clause).

7. Fiscal consolidation responsibility for states

The Committee observes that state government’s fiscal position is important after greater resource transfer to them (Fourteenth finance Commission award). Now, total state expenditures (as a percent of GSDP) is now even greater than the Centre. Hence, fiscal consolidation should also be made by the states. They should bring down their debt target to 20% of GDP from the current 21%.

8. Congruence of Fiscal and Monetary Policy

The FRBM Review Committee observed that both monetary and fiscal policies must ensure growth and macroeconomic stability in a complementary manner. For this, the Inflation Targeting (IT) regime and Fiscal Rules (FRs) have to interact with each other.

Source: TH

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

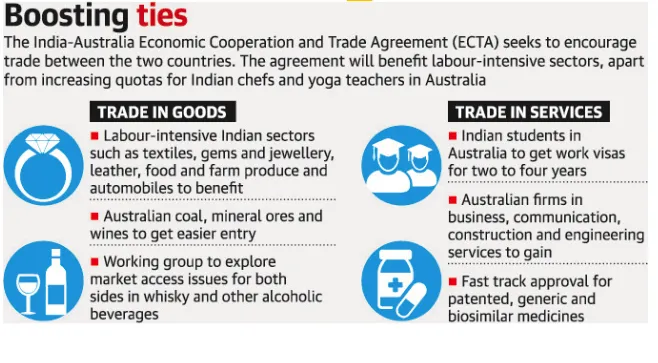

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

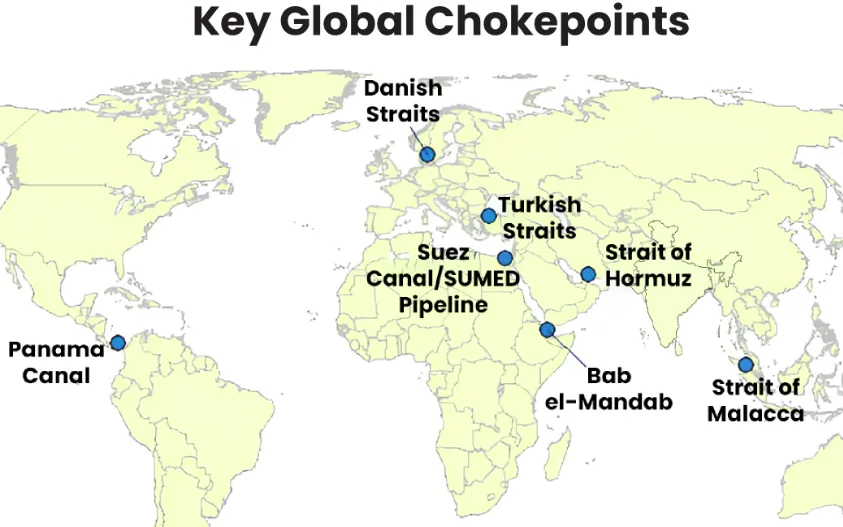

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment