Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

16 December, 2019

Min Read

Syllabus subtopic: Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment.

Prelims and mains focus: above the NPA crisis and the role of auditors in reporting bad loans; ethical standards related to auditing

News: India’s bad loan crisis seems far from over, with as many as 10 banks disclosing they had under-reported non-performing assets (NPAs) of close to 24,000 crore in the year ended 31 March.

These banks are State Bank of India (SBI), Yes Bank, Punjab National Bank, Central Bank of India, UCO Bank, Bank of India, Union Bank of India, Indian Overseas Bank, Indian Bank and Lakshmi Vilas Bank.

For India’s banks, saddled with bad loans of ?9.5 trillion, the findings by the Reserve Bank of India do not bode well.

Background

In 2017, the central bank directed banks to disclose the extent to which their assessment of NPAs and their provisioning diverged from that of RBI, and released guidelines for such classification. In April, RBI mandated banks to disclose information about provisioning divergence, if it exceeded 10% of a bank’s pre-provisioning profit.

Banks were also directed to disclose information if additional NPAs were more than 15 % of reported NPAs.

SBI’s case

The country’s largest lender, SBI, reported the largest bad loan divergence so far this year, under-reporting gross NPAs of ?11,932 crore. Divergence refers to the difference between what a bank reports as its bad loans and provisions, and what the central bank finds when auditing that bank’s books. SBI also reported divergence in provision of ?12,036 crore.

The bank disclosed the divergence to the stock exchange last week.

Earlier, SBI had reported its highest bad loan divergence of ?23,239 crore for 2016-17.

While loans turn bad once the repayment overdue exceeds 90 days, provision is the money set aside for each loan a bank disburses. Provisions mirror the change in an asset’s classification from standard to NPA and increase as the asset deteriorates.

Following these disclosures, experts have raised questions about the role of auditors in the reporting process.

Role of auditors in the regulation of bank accounts

From a regulatory perspective, auditors are the first line of defence, as bank accounts are prepared in accordance with the guidelines determined by RBI, with which bank auditors are well-versed. Hence, if the regulator RBI has detected misreported accounts, the auditors have to be held responsible and need to be penalized.

As banks hold unsecured deposits from the public, are highly leveraged and play a critical role in payments in the economy, they have to maintain the highest ethical standards. Indeed, by their very nature, banks are meant to stand for integrity and trust.

Is the fault only of auditors?

Lenders are not always at fault and the central bank would have sought NPA classification of some assets in retrospect and with abundant caution.

Not all divergences are a result of incorrect reporting or error of judgement.

In many cases, the stress in the account may have become apparent only in subsequent quarters after March ending. In such cases, it would be challenging for banks to pre-empt stress and, hence, report the such accounts as non-performing. Further, in many cases, divergent accounts would have been factored in the reported results of the first half of the year.

About NPAs (non-performing assets)

Classification of NPAs

Depending upon the period up to which a loan has remained as NPA, it is classified into three types:

Substandard Assets: An asset which remains as NPA for less than or equal to 12 months.

Doubtful Assets: An asset which remained in the above category for 12 months.

Loss Assets: These are assets where loss has been identified by the bank or the RBI. However, there may be some value remaining in it and hence the loan has not been not completely written off.

An example of NPA: Suppose State Bank of India (SBI) gives a loan of Rs. 5 crore to a company. They agreed upon for an interest rate of say 5 percent per annum. Now suppose that initially everything was good and the market forces were working in support of the company. In this scenario, the company was able to service the interest amount. Later, due to administrative, technical, legal, environmental, corporate reasons etc. suppose the company is not able to pay the interest rates for 90 days. In that case, a loan given to the company is a good case for the consideration as NPA.

Origin of the present NPA crisis:

The origin of the crisis lies partly in the credit boom of the years 2004-05 to 2008-09. In that period, commercial credit (‘non-food credit’) doubled.

It was a period in which the world economy as well as the Indian economy were booming. Indian firms borrowed furiously in order to avail of the growth opportunities they saw coming.

Most of the investment went into infrastructure and related areas: telecom, power, roads, aviation, steel. Businessmen were overcome with exuberance, partly rational and partly irrational. They believed, as many others did, that India had entered an era of 9% growth.

Thereafter, as the Economic Survey of 2016-17 notes:

Many things began to go wrong. Thanks to problems in acquiring land and getting environmental clearances, several projects got stalled. Their costs soared.

At the same time, with the onset of the global financial crisis in 2007-08 and the slowdown in growth after 2011-12, revenues fell well short of forecasts.

Financing costs rose as policy rates were tightened in India in response to the crisis. The depreciation of the rupee meant higher outflows for companies that had borrowed in foreign currency.

This combination of adverse factors made it difficult for companies to service their loans to Indian banks.

Source: mint

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

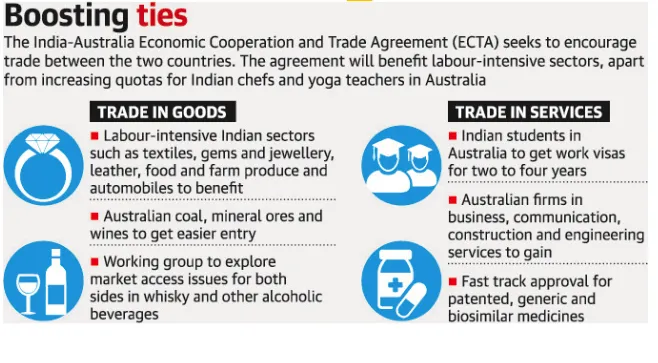

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

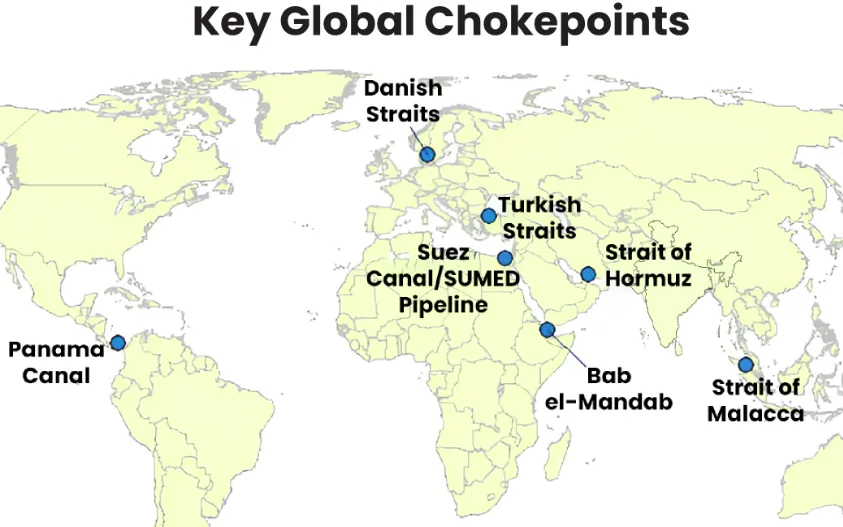

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment