Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

05 May, 2020

15 Min Read

By, Ramkishen S. Rajan is Yong Pung How Professor at Lee Kuan Yew School of Public Policy, National University of Singapore, and Sasidaran Gopalan is a Senior Research Fellow at the Nanyang Business School, Nanyang Technological University. Views are personal

Introduction

As the COVID-19 pandemic continues to ravage economies across the world, policymakers are desperately seeking effective ways to mitigate its economic effects.

The immediate future appears dire for large emerging markets including India, which recently saw its growth forecast for 2020 slashed by the International Monetary Fund (IMF) to 1.9% from the previously estimated 5.8%. In April, the World Bank estimated that India would grow 1.5% to 2.8% in 2020-2021, the lowest since the start of the 1991 economic reforms

Fiscal stimulus efforts

The Reserve Bank of India (RBI) has responded proactively and aggressively to ease liquidity concerns although the credit easing policy does not seem to have been transmitted yet to many firms.

It has also granted regulatory forbearance relating to asset classification to support economic activity, though some socialisation of losses might be inevitable over time.

In contrast, the Indian government’s fiscal stimulus efforts have paled in comparison to the rest of the world’s initiatives. India’s fiscal stimulus to date, estimated at ? 1.7 trillion, is less than 1% of the country’s GDP, which is paltry compared to the magnitude of stimulus injections undertaken by many East Asian countries such as Japan (20%), Malaysia (16.2%) and Singapore (12.2%).

Several observers have emphasised the need for India to roll out a revival package of at least 5% of the GDP (?10 trillion) to support the health and economic well-being of the most vulnerable (slum dwellers and migrant workers) as well as micro, small and medium-sized enterprises (MSMEs).

Relief packages in Asia

Most advanced economies can manage such financing by issuing bonds given their global demand. On the other hand, over 50 struggling low-income countries with limited resources to tackle the crisis have turned to the IMF for help.

The G7 countries have in principle agreed to offer debt relief to low-income countries by suspending their debt service payments.

The ones caught in between are mostly the middle-income emerging markets in Asia and elsewhere, like India. To date, the Asian Development Bank and the World Bank have committed to offering relief packages worth $1.5 billion and $1 billion, respectively, to India, while there are reports India has sought further multilateral assistance from the Asian Infrastructure Investment Bank.

However, with a government debt of around 72% of GDP, which is comparatively higher than all other emerging markets in the region, India’s fiscal room to opt for a massive stimulus appears much more limited.

Any aggressive stimulus spending will not only result in a surge in India’s gross public debt but will also negatively impact its credit ratings.

Even if the Fiscal Responsibility and Budget Management constraints are relaxed, given India’s limited demand for domestic bonds, there is a need to seek capital flows to finance its additional stimulus by encouraging foreign investment in government securities.

Some richer countries in the Asian region like Singapore have managed to tap into their deep reserve kitty benefiting from the significant role played by their sovereign wealth funds.

While India does not have that luxury, it has been suggested that some of the country’s $476 billion of foreign exchange (FX) reserves be used towards this purpose.

This is an extremely risky option in light of India’s sizeable current account deficits and heavy dependence on short-term capital inflows. Given the likely pressure on its balance of payments moving forward, utilising FX reserves does not seem to be viable at the moment.

A radical financing option would be to monetise the deficits by allowing the RBI to print money to buy the government bonds as long as inflation remains under check, though this might set a dangerous precedent (something the RBI stopped doing in 1997) moving forward. India has worked hard to move away from such money-financed fiscal stimulus policies that led to weak budget constraints and macroeconomic instability.

Adequate fiscal space

Unless there is proper governance of any massive fiscal spending, even a very well-intentioned policy may end up doing more harm than good. Even countries like China have been guarded in their fiscal responses so far. In China, this was partly to avoid a rise in its shadow banking activities, which turned out to be one of the perverse side-effects of its massive stimulus post the global financial crisis.

Countries with higher initial public debt levels like India need to be particularly concerned as they also happen to possess the least state capacity to make tough decisions to return to a trajectory of fiscal credibility.

Way ahead

There is clearly a need to start re-prioritising expenditures away from low-priority, unproductive areas towards greater spending on health and social safety nets for low-income households.

Source: TH

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

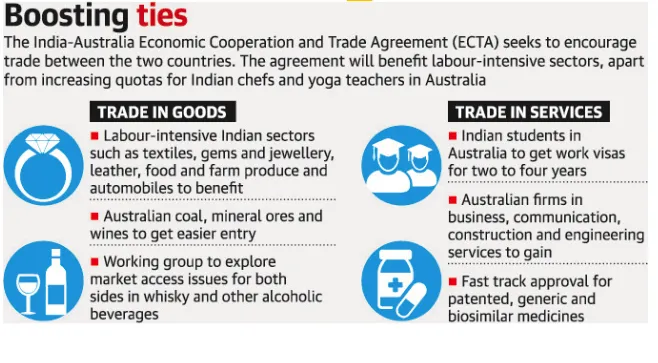

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

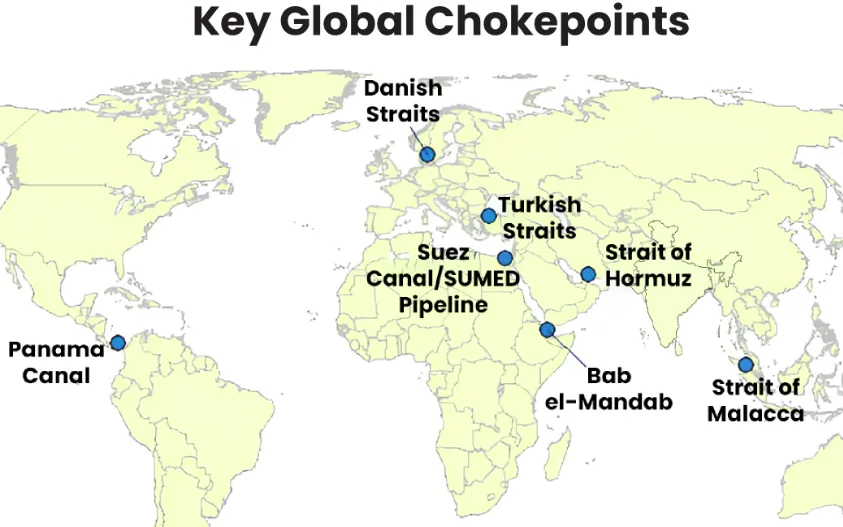

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment