Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

03 February, 2026

6 Min Read

NITI Aayog has released a report titled “Deepening the Corporate Bond Market in India”, emphasizing that an efficient and liquid corporate bond market is essential for expanding market access, improving liquidity, and enhancing investor participation. The report highlights the need for coordinated reforms to unlock the market’s full potential and support India’s long-term economic growth.

Overview and Key Highlights of the Report

India’s corporate bond market has witnessed significant expansion over the last decade. However, it continues to remain shallow and illiquid due to regulatory overlap, restrictive investment mandates, delays in insolvency resolution, and weak risk-management infrastructure.

NITI Aayog recommends a six-year reform roadmap focusing on regulatory simplification, product innovation, and technological integration, with the goal of building a ?100–120 trillion corporate bond market by 2030.

Current State of India’s Corporate Bond Market

Growth with Untapped Potential

India’s corporate bond market expanded from ?17.5 trillion in FY2015 to ?53.6 trillion in FY2025, registering a compound annual growth rate (CAGR) of nearly 12%. Despite this progress, the market size remains modest at 15–16% of GDP, significantly lower than peer economies such as South Korea (79%) and Malaysia (54%).

Concentration and Limited Participation

Bond-based fundraising has become comparable to bank credit; however, the market is highly concentrated. Nearly 98% of issuances occur through private placements, largely by AAA- and AA-rated corporates. Participation from MSMEs, retail investors (less than 2%), and foreign portfolio investors remains limited.

Liquidity Constraints

The secondary corporate bond market is illiquid, with a low annual turnover ratio of around 0.3. This is largely due to a buy-and-hold strategy adopted by institutional investors such as insurance companies and pension funds.

Future Potential

With sustained reforms and innovation, India’s corporate bond market has the potential to grow beyond ?100–120 trillion by 2030, emerging as a key pillar of financial stability and economic growth.

Why a Deep Corporate Bond Market is Essential for India

Supporting Viksit Bharat 2047

India’s aspiration to become a USD 30 trillion economy with a per capita income of USD 18,000 by 2047 requires a financial system capable of mobilising large volumes of long-term, low-cost capital.

Balanced Financial Architecture

A deep bond market provides an alternative to bank financing, broadens funding avenues, lowers borrowing costs, and creates a competitive and liquid environment where diverse issuers can directly access long-term capital.

Driving Capital Formation

Corporate bonds channel institutional and household savings into productive investments and facilitate the development of risk-management instruments such as credit derivatives and securitisation.

Reducing Banking Sector Stress

Diversified funding sources reduce excessive dependence on banks, allowing them to focus on priority sectors and MSMEs, while also mitigating non-performing asset (NPA) and credit concentration risks.

Strengthening Monetary Policy Transmission

A deep bond market enhances the effectiveness of monetary policy by enabling faster and more transparent interest rate transmission through a well-defined yield curve, which also serves as a benchmark for pricing credit risk across the economy.

Key Challenges in Developing a Deep Corporate Bond Market

Regulatory Overlap and Complexity

The involvement of multiple regulators—SEBI, RBI, and the Ministry of Corporate Affairs—creates fragmented compliance requirements, higher costs, and procedural delays, particularly for new financial instruments.

Restrictive Investment Mandates

Insurance companies and pension funds are often mandated to invest primarily in high-rated bonds, restricting capital flow to lower-rated but productive corporates.

Weak Investor Protection

Limited enforcement capacity of debenture trustees and gaps in bondholder protection reduce investor confidence, especially in lower-rated debt instruments.

Inefficient Insolvency Resolution

Although the Insolvency and Bankruptcy Code (IBC) exists, resolution processes face delays, with an average duration of 713 days against the mandated 330 days, alongside declining recovery rates.

High Costs and Tax Disincentives

High issuance and listing costs, complex TDS rules on interest income, and less favourable capital gains tax treatment compared to equities reduce the attractiveness of corporate bonds.

Underdeveloped Market Ecosystem

Shallow markets for credit default swaps, securities lending, and fragmented data infrastructure limit price transparency and hinder effective risk assessment and trading activity.

Reforms Undertaken to Strengthen the Corporate Bond Market

Reserve Bank of India (RBI) Initiatives

The RBI has introduced measures such as tri-party repos, Partial Credit Enhancement (PCE), the Retail Direct platform, and the Voluntary Retention Route (VRR) for foreign portfolio investors.

Government Measures

The government enacted the Insolvency and Bankruptcy Code, launched the Corporate Debt Market Development Fund (CDMDF) as a safety net, and promoted municipal bonds under AMRUT 2.0.

Parliamentary Recommendations

A Select Committee of the Lok Sabha has recommended a three-month time limit for insolvency appeals at the NCLAT, inclusion of registered valuers as service providers under the IBC, and allowing multiple resolution plans during the corporate insolvency resolution process.

NITI Aayog’s Proposed Roadmap for Deepening the Market

NITI Aayog proposes a three-phase reform strategy over six years, aimed at strengthening market foundations before advancing towards global integration.

Phase I (1–2 Years): Strengthening Foundations

This phase focuses on regulatory streamlining across SEBI, RBI, and MCA; improving retail participation through digital platforms and investor education; strengthening debenture trustees; improving insolvency timelines; piloting AI-driven credit scoring for SMEs; and encouraging voluntary market-making.

Phase II (2–4 Years): Expansion and Innovation

This phase proposes the introduction of innovative instruments such as covered bonds, targeted subsidy bonds, and fractional bond funds. It also includes creating dedicated platforms for SME and lower-rated bonds and reviewing investment mandates of institutional investors to allow greater diversification.

Phase III (4–6 Years): Integration and Maturity

The final phase envisages establishing a unified bond market regulator or a high-powered statutory task force, leveraging advanced technologies like blockchain and artificial intelligence, and gradually integrating India’s bond market with global settlement systems such as Euroclear.

Conclusion

India’s corporate bond market has grown substantially but remains fragmented and shallow, limiting its role in financing long-term development. Coordinated reforms in regulation, investor diversification, insolvency efficiency, and market infrastructure are essential to transform it into a ?100–120 trillion financing pillar, supporting financial stability and the vision of Viksit Bharat 2047.

Source: INDIAN EXPRESS

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

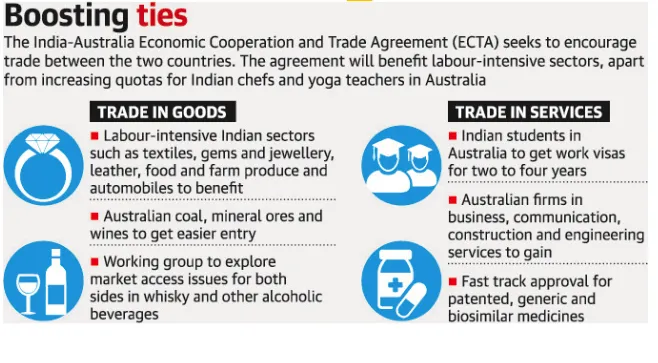

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

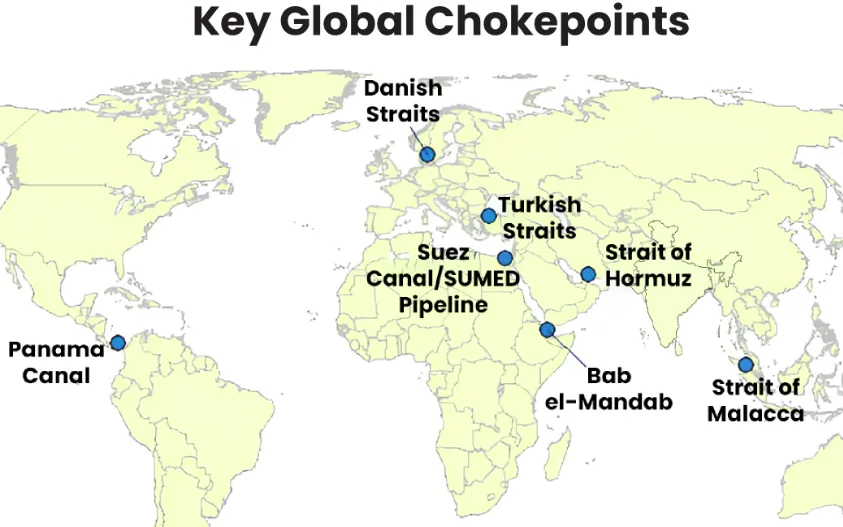

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment