Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

17 March, 2026

4 Min Read

India’s aviation sector has grown rapidly, becoming a major economic success story. However, regulatory oversight has not evolved at the same pace. Data-driven monitoring of fares and market behavior is essential to ensure fair competition, prevent market abuse, and shift from reactive crisis management to proactive regulation.

Challenges in the Current Regulatory Framework

Slow Regulatory Data Systems

Passenger traffic has expanded rapidly, low-cost carriers dominate domestic skies, and airport infrastructure is growing in metros and tier-2 cities. However, regulatory data systems have lagged, leaving authorities with limited insights into market dynamics.

Largely Volume-Focused Oversight

Current oversight primarily tracks passenger numbers, fleet size, and freight traffic. There is little focus on fare behavior or market conduct, creating vulnerabilities in an increasingly algorithm-driven and complex sector.

Prices in a Dynamic Market

Airline fares fluctuate in real time due to demand patterns, seat availability, competitor pricing, seasonal factors, and route-specific market share. Distinguishing legitimate fare changes from exploitative pricing is difficult without detailed data.

Limits of Crisis-Based Regulation

Temporary interventions such as price caps or post-crisis investigations have been the norm. These measures provide only short-term relief and cannot replace continuous, analytical oversight. Retrospective data is often limited and insufficient for detecting anti-competitive practices.

Why Data Transparency Matters

Data transparency enables regulators to detect structural and market issues. Key benefits include:

Identifying Route-Level Market Power: Routes dominated by a single airline often show higher fares, signaling potential abuse of dominance.

Tracking Entry and Exit Effects: Monitoring fare changes when competitors enter or exit a route reveals competitive intensity.

Monitoring Peak-Period Pricing: High-demand periods provide natural tests; disproportionate fare increases by dominant airlines may indicate exploitation.

Encouraging Algorithmic Accountability: Observable pricing outcomes encourage airlines to build compliance safeguards into revenue management systems.

Structured data acts as a deterrent, reducing the need for constant intervention.

Learning from Global Best Practices

The United States’ DB1B Model offers a valuable reference:

The Bureau of Transportation Statistics (BTS) maintains the Airline Origin and Destination Survey (DB1B), which collects a 10% random sample of all domestic tickets each quarter. This includes fares, routes, and carrier details. Benefits of this approach include:

Monitoring long-term pricing trends

Supporting empirical research

Strengthening competition oversight

Promoting market transparency

For India, adopting a similar 10% sampling framework would shift the focus from volume tracking to systematic market behavior monitoring.

Addressing Industry Concerns

Resistance to data transparency often focuses on three areas:

Proprietary Algorithms: Airlines worry about revealing their “secret sauce.” Sampling ticket data monitors outcomes without exposing algorithms.

Technical Burden: Submitting a fraction of ticket data quarterly is manageable given existing digital infrastructure.

Risk of Implicit Coordination: Quarterly and delayed data releases minimize the risk of competitor coordination while retaining regulatory value.

Moving from Reactive Controls to Institutional Strength

India’s aviation future depends not just on expanding fleets and airports but also on regulatory sophistication. A data-first approach would:

Reduce reliance on ad hoc fare caps

Improve competition oversight

Strengthen consumer confidence

Support evidence-based policymaking

As aviation becomes increasingly algorithm-driven, regulation must become analytical to keep pace.

Conclusion

India’s aviation sector is a major economic success story. However, rapid growth without robust data infrastructure risks regulatory blind spots. The solution lies in structured transparency, not heavy-handed control. In a market of India’s scale, data-driven oversight is critical for sustainable, fair, and competitive growth.

Source: INDIAN EXPRESS

28 February, 2026

4 Min Read

Recent events have highlighted systemic vulnerabilities in India’s civil aviation:

Ahmedabad Plane Crash (June 2025): A tragic accident that exposed operational and safety risks.

IndiGo Flight Cancellations (December 2025): Large-scale cancellations and delays revealed that aviation problems are no longer temporary or airline-specific.

Overview of India’s Civil Aviation

India has emerged as one of the fastest-growing aviation markets, currently ranked third globally in domestic air travel.

The sector operates over 840 aircraft, carrying more than 350 million passengers annually.

Air travel has transitioned from a luxury to an essential mode of transport due to rising incomes, growing middle-class aspirations, and improved regional connectivity.

Drivers of Domestic Aviation Growth

Rising Disposable Income: More people can afford air travel.

Low-Cost Carrier Dominance: Airlines such as IndiGo make flying affordable for the masses.

Infrastructure Development: New airports and terminal expansions improve connectivity.

Government Initiatives:

UDAN Scheme (Ude Desh ka Aam Nagrik): Operationalised hundreds of regional routes, connecting Tier-2 and Tier-3 cities.

Projections:

Domestic passenger traffic is expected to reach 715 million by 2030.

Pilot demand is projected at 7,000 between 2024–26, increasing to 25,000–30,000 over the next decade.

Key Issues in India’s Civil Aviation

1. Pilot Shortage and Training Bottlenecks

India has a lower pilot-to-aircraft ratio (14–16 pilots per aircraft) compared to the global benchmark of 18–20.

Limited simulator capacity, high training costs, and shortage of instructors restrict new pilot production.

2. Stricter Flight Duty Time Limitations (FDTL)

Reduced night operations and mandatory rest periods expose scheduling vulnerabilities.

3. Market Concentration (Duopoly Risk)

IndiGo and Air India control nearly 90% of domestic passenger traffic, creating connectivity risks when a dominant carrier faces disruption.

4. Financial Fragility

Intense fare competition, high operating costs, and fluctuating aviation fuel prices reduce profitability.

Past airline collapses reflect structural financial instability.

5. Infrastructure Constraints

Major airports like Delhi and Mumbai operate near full capacity, causing slot shortages and congestion.

Many regional airports lack night landing facilities, modern navigation systems, and adequate passenger amenities.

6. Regulatory Oversight Challenges

DGCA vacancies in technical and safety positions reduce effective oversight.

Temporary exemptions often manage disruptions instead of systemic corrections.

7. Overutilisation of Assets

Airlines operate with high aircraft utilisation, minimal spare crew, and tight turnaround schedules, leaving little buffer for disruptions.

8. Regional Airline Sustainability

New regional carriers face weak demand, high costs, competition from dominant carriers, and fuel/currency volatility, leading to past failures.

9. Rising Demand vs System Readiness

India accounts for >4% of global air traffic, with passenger numbers projected to more than double by 2030.

However, training, regulatory capacity, infrastructure, and safety buffers remain insufficient.

Efforts and Initiatives to Address Challenges

1. Strengthening Pilot Availability and Training

New Flying Training Organisations (FTOs) established to increase Commercial Pilot Licence output and reduce reliance on foreign academies.

2. Phased Implementation of Revised FDTL Norms

Aims to reduce pilot fatigue and align safety standards with global best practices.

3. Development of Greenfield Airports

Examples: Noida International Airport (Jewar), Navi Mumbai International Airport.

Expected to reduce congestion, increase slot availability, and support regional growth.

4. Modernisation of Existing Airports

PPP initiatives for terminal expansion, runway upgrades, and improved passenger facilities.

5. Promotion of Regional Connectivity (UDAN Scheme)

Features Viability Gap Funding (VGF), reduced airport charges, and revival of unserved/underserved airports.

6. Encouraging Market Competition

Issuance of NOCs to new regional airlines to reduce dependence on dominant carriers and improve connectivity.

7. Enhancing Regulatory Oversight

Filling DGCA technical vacancies, intensifying audits, inspections, and monitoring compliance with FDTL and safety standards.

8. Financial and Structural Reforms

Mergers like Vistara into Air India create financially robust entities.

New-generation aircraft improve fuel efficiency, reduce operating costs, and enhance environmental performance.

9. Improving Operational Resilience

Gradual reassessment of crew-to-aircraft ratios and promotion of domestic MRO facilities to reduce downtime.

10. Air Traffic Management Modernisation

Investments in GAGAN satellite navigation, advanced air traffic systems, and airspace redesign to reduce congestion and enhance safety.

11. Temporary Liberalised Hiring of Foreign Pilots

Short-term measure to address pilot shortages and ensure operational continuity.

Conclusion

India’s aviation sector is at a critical juncture, facing high market concentration, pilot shortages, stretched regulatory capacity, and rising safety risks.

The sector must shift from aggressive expansion to resilience-building.

Delays in corrective measures will impact passengers, airline stability, and national credibility.

Source: INDIAN EXPRESS

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

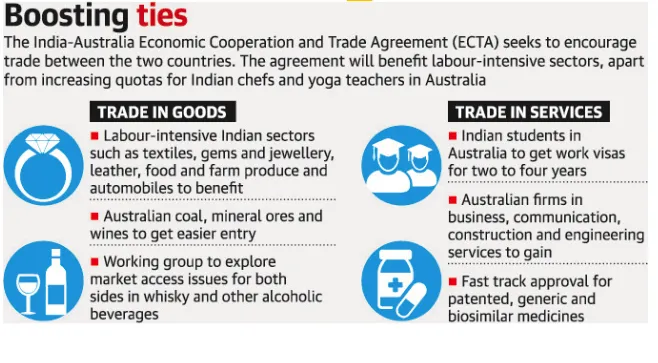

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

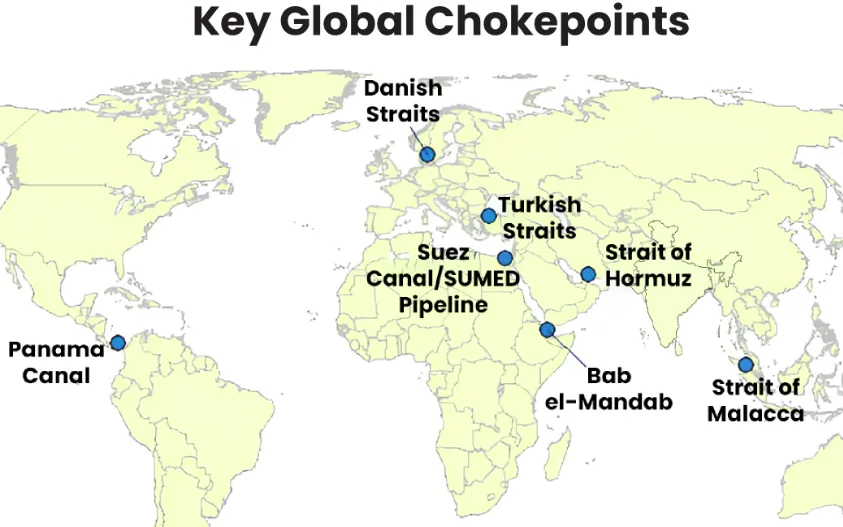

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment