Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

09 May, 2020

10 Min Read

By, C. Rangarajan is former Chairman, the Prime Minister’s Economic Advisory Council and Former Governor, Reserve Bank of India. D.K. Srivastava is Chief Policy Advisor, EY India and former Director, Madras School of Economics. The views expressed are personal

Introduction

Various institutions have assessed India’s growth prospects for 2020-21 ranging from 0.8% (Fitch) to 4.0% (Asian Development Bank).

The International Monetary Fund (IMF) has projected India’s growth at 1.9%, China’s at 1.2%, and the global growth at (-) 3.0%.

The actual growth outcome for India would depend on:

1. the speed at which the economy is opened up;

2. the time it takes to contain the spread of the virus, and

3. the government’s policy support.

Growth prospects

India slid into the novel coronavirus crisis on the back of a persistent economic downslide. There was a sustained fall in the saving and investment rates with unutilised capacity in the industrial sector.

In 2019-20, there was a contraction in the Centre’s gross tax revenues in the first 11 months from April 2019 to February 2020, at (-) 0.8%. These trends continue to beset the Indian economy in this crisis.

We examine the growth prospects for 2020-21 from the output side, making reference to real gross value added (GVA).

In 2019-20, which would serve as the base year, India may show GVA growth of about 4.4%, well below the Central Statistics Office’s second advance estimate of 4.9%, as the fourth quarter number is likely to be revised downwards on account of the adverse impact of the virus on economic activities. The IMF’s GDP growth estimate for 2019-20 is 4.2%.

GVA is divided into eight broad sectors. Although all sectors have been disrupted, some may be affected less than others.

We divide the output sectors into four groups.

1. In group A, we consider two sectors that have suffered only limited disruption — namely agriculture and allied sectors, and public administration, defence and other services.

# In the case of agriculture, rabi crop is currently being harvested and a good monsoon is predicted for later in the year. Despite some labour shortage issues, this sector may show near-normal performance.

# The public and defence services have been nearly fully active, with the health services at the forefront of the COVID-19 fight.

For the group A sectors, it may be possible to achieve 90% of the 2019-20 growth performance.

2. Group D includes trade, hotels, restaurants, travel and tourism under the broad group of “Trade, Hotels, Transport, Storage and Communications”.

This sector may be able to show 30% of 2019-20 growth performance.

3. Group B comprises four sectors which may suffer average disruption showing 50% of 2019-20 growth performance.

These sectors are mining and quarrying, electricity, gas, water supply and other utility services, construction, and financial, real estate and professional services.

4. In the last group (Group C), we place manufacturing which has suffered significant growth erosion in 2019-20. It is feasible to stimulate this sector by supporting demand.

In this case, we apply a 40% performance factor, not on the 2019-20 growth which is an outlier, but on the average growth of the preceding three years. Considering these four groups together, a GVA growth of 2.9% is estimated for 2020-21.

Realising this requires strong policy support, particularly for the manufacturing sector which has a weight of 17.4%. It is also based on the assumption that the Indian economy may move on to positive growth after the first quarter. In the first quarter, GVA growth will be negative.

Calibrating policy support

Monetary policy initiatives undertaken so far include a reduction in the repo rate to 4.4%, the reverse repo rate to 3.75%, and the cash reserve ratio to 3%.

The Reserve Bank of India has also opened several special financing facilities.

These measures need to be supplemented by an appropriate fiscal stimulus.

Although the industry has been clamouring for a large fiscal stimulus, cash-constrained Central and State governments have taken expenditure-reducing measures by announcing the freezing of enhancements of dearness allowance and dearness relief.

This may result in savings of? 37,000 crore for the Centre and about? 82,000 crore for the States, together amounting to 0.6% of GDP.

There is also a talk of substantially reducing non-salary defence expenditure. With lower petroleum prices, fertilizer and petroleum subsidies may be reduced. These expenditure cuts are contemplated to keep the fiscal deficit under some control.

On fiscal deficit

Fiscal stimulus can be of three types:

(a) Relief expenditure for protecting the poor and the marginalised;

(b) Demand-supporting expenditure for increasing personal disposable incomes or government’s purchases of goods and services, including expanded health-care expenditure imposed by the novel coronavirus, and,

(c) Bailouts for industry and financial institutions.

The Centre had earlier announced a relief package of ?1.7-lakh crore of which the additionality was only ? 65,000 crore, since it included a frontloading of the budgeted expenditures.

The Centre’s budgeted fiscal deficit of 3.5% of GDP may have to be enhanced substantially to make up for the shortfall in budgeted revenues; account for a lower than projected nominal GDP for 2020-21, and provide for a stimulus.

Thus, the Centre’s fiscal deficit may increase to 6.0% of GDP.

Expenditure on the construction of hospitals, roads and other infrastructure and the purchase of health-related equipment and medicines require prioritisation.

These expenditures will have high multiplier effects.

Similar initiatives may be undertaken by the State governments which may also enhance their combined fiscal deficit to about 4.0% of GDP to account for 3.0% of GDP under their respective Fiscal Responsibility Legislation/Law and to provide for the shortfall in their revenues and some stimulus.

Financing of the fiscal deficit poses a major challenge this year. On the demand side, the Central (6.0%) and State governments (4.0%) and Central and State public sector undertakings (3.5%) together present a total public sector borrowing requirement (PSBR) of 13.5% of GDP.

Against this, the total available resources may at best be 9.5% of GDP consisting of excess savings of the private sector at 7.0%, public sector saving of 1.5%, and net capital inflow of 1.0% of GDP3.

The gap of 4.0% points of GDP may result in an increased cost of borrowing for the Central and State governments.

This gap may be bridged by enhancing net capital inflows including borrowing from abroad and by monetising some part of the Centre’s deficit. The monetisation of debt can at best be a one-time effort. This cannot become a general practice.

Source: TH

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

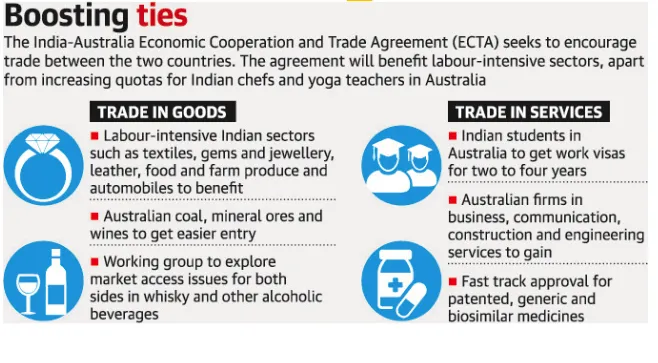

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

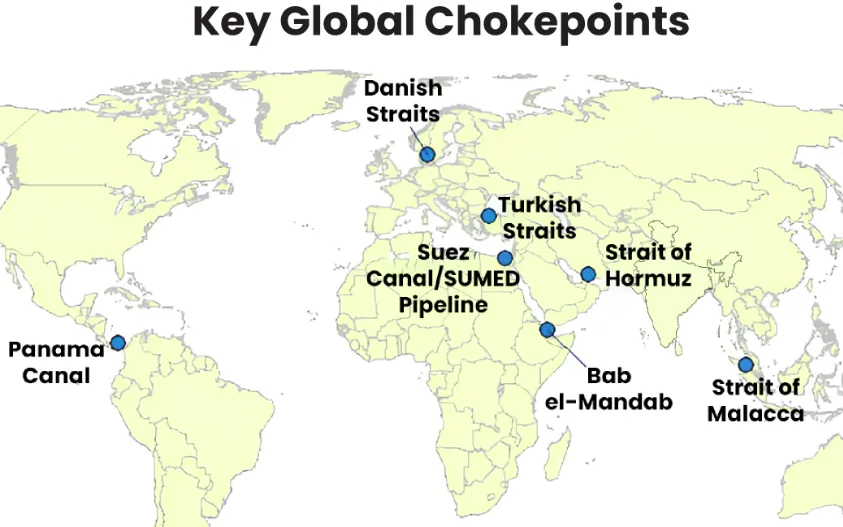

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment