Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

06 September, 2025

4 Min Read

A cess is an additional tax imposed by the Government of India for a specific purpose, as authorized under Article 270 of the Indian Constitution. It is levied on top of existing taxes or duties listed in the Union List of the Seventh Schedule of the Constitution.

Key Features of a Cess:

Examples of Cess:

Surcharge: An Additional Levy

Differences between Cess and Surcharge:

|

Aspect |

Tax |

Cess |

Surcharge |

|

Definition |

A levy imposed on income, property, or transactions (e.g., income tax, GST). |

An additional levy for a specific purpose, imposed on existing taxes (e.g., Education Cess, Swachh Bharat Cess). |

An additional levy on existing taxes, generally progressive in nature (e.g., income tax surcharge). |

|

Revenue Use |

Goes to the Consolidated Fund, used generally. |

Credited to the Consolidated Fund but used only for a specific purpose. |

Credited to the Consolidated Fund and used generally, without a specific purpose restriction. |

|

State Sharing |

Shared with states as part of the divisible pool. |

Not shared with states, remains with the Centre. |

Not shared with states, remains with the Centre. |

|

Examples |

Income Tax, Corporate Tax, GST. |

Swachh Bharat Cess, Education Cess, Krishi Kalyan Cess. |

Income tax surcharge, Corporate tax surcharge. |

CAG’s Flagged Shortfall in Cess Transfer

The Comptroller and Auditor General (CAG) raised concerns about the Rs 3.69 lakh crore shortfall in transferring the cess collections to their intended funds. This highlights an important issue in the functioning of cess funds and their proper utilisation.

Implications:

Conclusion

Cess and surcharge are distinct in terms of their purpose, usage, and impact on Union finances. While both are credited to the Consolidated Fund of India and are not shared with states, cess must be strictly used for its intended purpose, unlike the surcharge which is used for general government expenditure. The issue of Rs 3.69 lakh crore shortfall in transferring cess collections to their designated funds, as flagged by the CAG, raises concerns over the proper utilisation of these levies, which are supposed to serve specific purposes like education, sanitation, and agriculture. It underscores the need for better oversight and accountability in the management of such funds

Source: PIB

24 August, 2025

4 Min Read

The Comptroller and Auditor General (CAG) has reported that, as of 2023-24, the Central Government has failed to transfer ?3.69 lakh crore worth of cess collections to the relevant funds for which the cess was implemented.

A cess is a form of additional tax levied by the government for a specific purpose. It's different from regular taxes like excise duties or income tax, as it is a supplementary charge added on top of existing taxes.

Purpose: Cess is implemented for specific objectives, such as cleanliness, education, or other welfare activities, until the government accumulates sufficient funds for that purpose.

Example: The Swachh Bharat cess, introduced for cleanliness initiatives across India, is a well-known case.

Tax on Tax: A cess is an extra tax, meaning it is applied in addition to the standard taxes that individuals and businesses already pay. For example, someone who pays income tax may also pay a cess for a specified purpose.

Unlike general tax revenues, which are pooled into the Consolidated Fund of India (CFI) and used for any government expenditure, the proceeds from cess must be appropriated by Parliament and spent only on the designated purposes for which the cess was levied.

There are some nuances in how the funds are utilized:

While tax revenues are typically shared with state governments, cess revenues may not be shared with them, which limits their direct benefit from such funds.

Purpose: Taxes fund general government expenses, while cess is aimed at funding a specific purpose.

Revenue Usage: While tax revenue goes to the Consolidated Fund of India for general use, cess revenue is meant to be used only for the specific goal it was levied for, after parliamentary approval.

Distribution: Taxes are shared between the Center and States, but cess may not necessarily be shared.

The failure to transfer cess funds has raised concerns regarding government transparency and accountability in fund management. The ?3.69 lakh crore collected has not been appropriately allocated to the specified projects, which may have serious implications for the intended development programs.

While cess is a critical tool for funding specific initiatives, the non-transfer of funds to the relevant schemes highlights the need for more effective financial management. It also calls into question the government’s commitment to the intended purposes behind these additional taxes.

Source: PIB

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

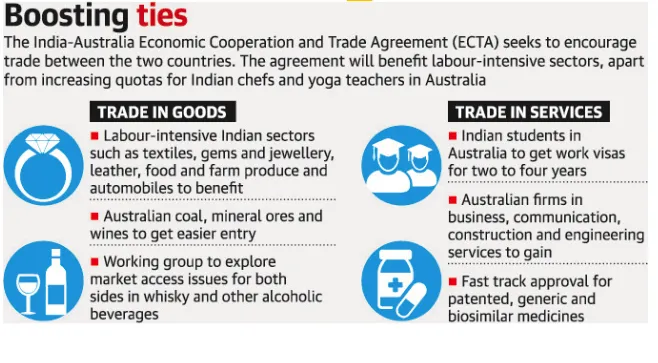

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

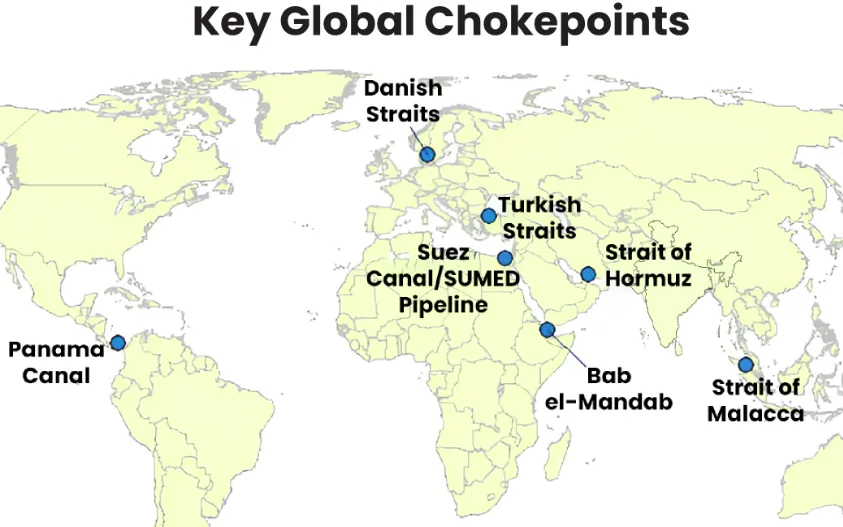

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment