Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

20 February, 2026

4 Min Read

Recently, the Reserve Bank of India (RBI) released a discussion paper inviting public comments on the issuance of new licences for cooperative banks. This has revived the long-standing debate on whether cooperative banks can be effectively regulated within India’s modern, prudential banking framework. The issue is not merely about licensing but about reconciling cooperative principles with contemporary banking regulation.

About Cooperative Banks

Cooperative banks are member-owned and democratically governed institutions built on the principles of open membership, democratic control (one member, one vote), and mutuality.

Historically, they have played a crucial developmental role in rural and semi-urban India by:

Providing affordable credit and savings facilities,

Serving communities excluded from mainstream banking, and

Operating on the basis of local trust and lower transaction costs.

The All-India Rural Credit Survey Committee (1954) famously observed that “if co-operatives fail, there fails the last hope of rural India.” This highlights their importance in promoting financial inclusion and grassroots development.

Current Status of Cooperative Banks

As of March 31, 2025, India had 838 cooperative banks, each with deposits below ?100 crore. No new cooperative bank licences have been issued since 2001, although the idea resurfaces periodically.

The sector remains small, fragmented, and locally concentrated, making supervision complex. Unlike large commercial banks such as State Bank of India, which can be regulated through system-based and risk-based supervision, cooperative banks require individualised oversight, thereby increasing the regulatory burden.

Structural Issues and Concerns

1. Structural Mismatch

A fundamental issue lies in the nature of cooperative capital. Share capital in cooperatives is withdrawable and linked to membership, making it behave more like a deposit than stable regulatory capital.

This structure is incompatible with the capital-centric prudential norms under the Banking Regulation Act. Hence, there is a mismatch between cooperative design and modern banking regulation.

2. Scale vs. Mutuality

True cooperatives are meant to be small, neighbourhood-based institutions. However, modern banking requires scale to provide services such as remittances, credit cards, export credit, and corporate finance.

Thus, a “cooperative bank” becomes an apparent contradiction — too small to achieve efficiency, yet too large to preserve genuine cooperative character.

3. Governance Challenges

Democratic governance allows borrower-members to sit on boards, which can weaken professional decision-making. In many large cooperative banks:

Membership is effectively closed,

Non-member business dominates, and

Cooperative principles are diluted.

This raises concerns about political interference, weak management, and governance failures.

4. Regulatory Burden and Backdoor Licensing

Issuing new licences may lead to a proliferation of small, unitary institutions requiring direct supervision by the RBI.

There is also concern that cooperative licences may become a backdoor route for promoters who do not qualify for universal banking licences. The RBI thus faces a paradox: institutions that are too small to regulate efficiently, yet too large to remain genuine cooperatives.

Committee Recommendations: Divergent Approaches

Malegam Committee (2011)

The Malegam Committee supported the issuance of new licences, provided strict eligibility and prudential norms were applied. It emphasised sound governance, capital adequacy, and viability, arguing that the cooperative form alone should not disqualify institutions.

R Gandhi Committee (2015)

The R Gandhi Committee recommended resuming licences within a well-defined and differentiated regulatory framework. It proposed a four-tier structure, stricter governance norms, and encouraged consolidation and conversion of strong entities into small finance banks.

Vishwanathan Committee (2021)

The Vishwanathan Committee adopted a cautious approach, especially after failures such as Punjab and Maharashtra Cooperative Bank. It recommended focusing on strengthening existing banks, improving governance, and encouraging consolidation, rather than aggressive new licensing.

In summary, earlier committees favoured expansion with safeguards, while the latest committee prioritised stability and reform over expansion.

Reform Measures Undertaken

Amendments to the Banking Regulation Act have strengthened the RBI’s supervisory powers over cooperative banks and reduced dual regulation between the Centre and States.

Additionally, the creation of an Umbrella Organisation (UO) aims to provide shared services and lay the foundation for a federated cooperative structure.

Way Forward

1. Adopt a Federated Cooperative Model

India can move toward a federated structure, where:

Primary cooperatives handle local customer relationships,

National-level federations manage capital, technology, treasury, and compliance.

This would ensure stable capital at the top and inclusion at the grassroots.

2. Affiliate Rather Than Multiply

Instead of issuing numerous new licences, smaller cooperative banks can affiliate with well-capitalised federal institutions. Weak, single-branch banks may be converted into cooperative societies with cancelled banking licences.

3. Ease Regulatory Burden

Fewer but stronger institutions would allow the RBI to adopt risk-based supervision, reducing systemic risk while preserving financial inclusion.

Conclusion

Cooperatives remain vital instruments of financial inclusion in India. However, cooperative banks in their present structure face serious governance, capital, and regulatory challenges.

The Reserve Bank of India stands at a critical juncture: it can either continue with incremental licensing or undertake a structural redesign through a federated, future-ready cooperative banking model.

The central question is not whether cooperatives matter — they undoubtedly do — but whether India can reform cooperative banking to make it both inclusive and systemically sound.

Source: INDIAN EXPRESS

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

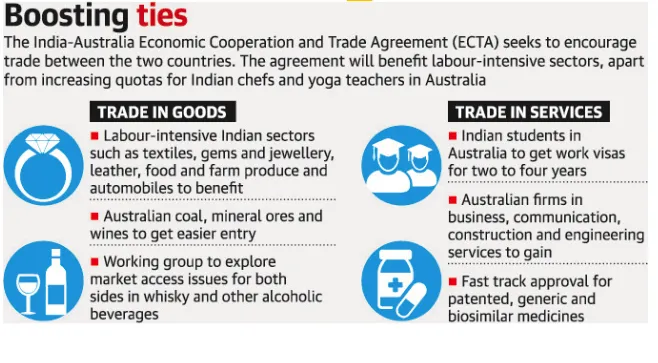

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

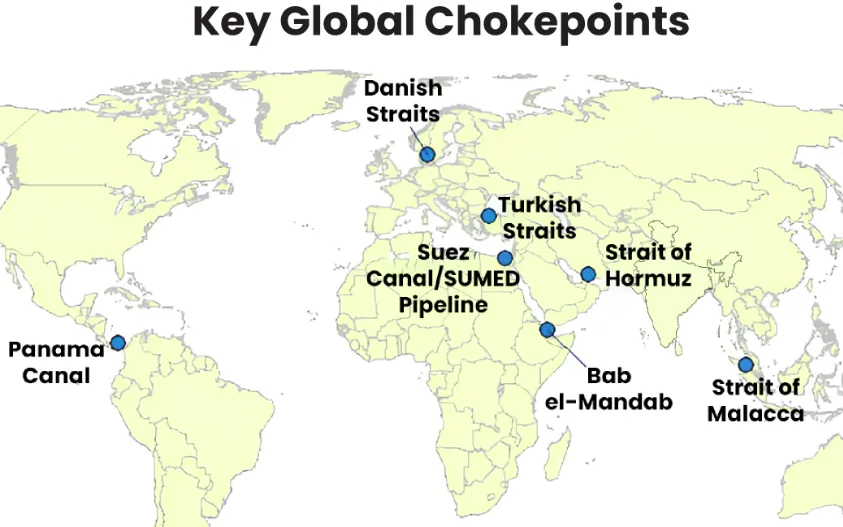

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment