Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

18 January, 2022

15 Min Read

Source: TH

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

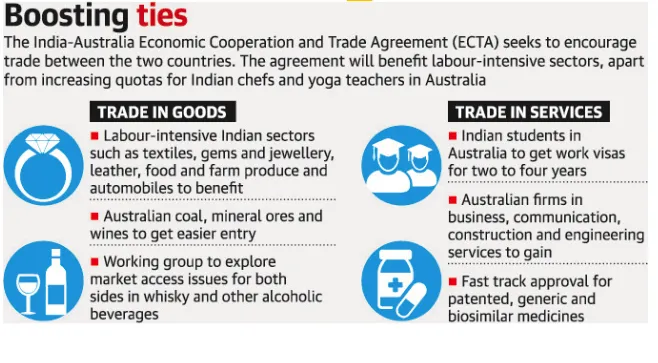

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

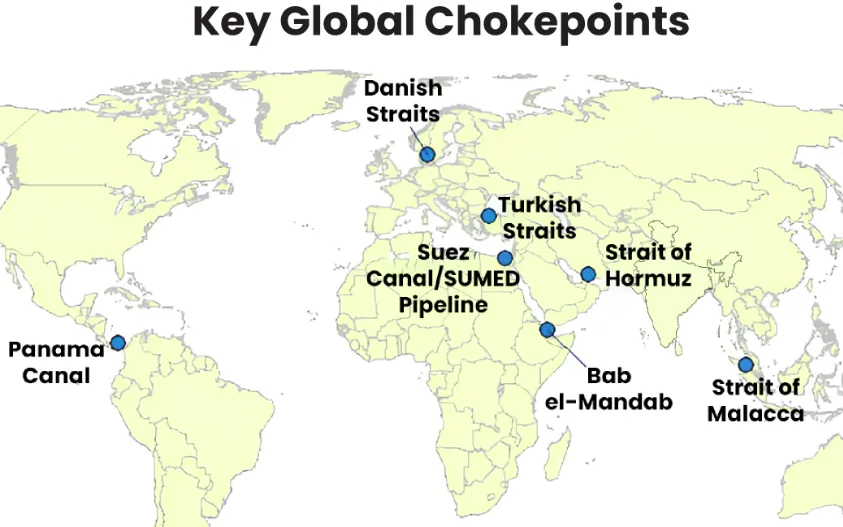

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment