Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

26 March, 2020

6 Min Read

Part of: GS Prelims and GS-III- Economics

Recently, the Centre has approved a ?1,340-crore recapitalisation plan for Regional Rural Banks (RRBs). The move is crucial to ensure liquidity in rural areas during the lockdown due to the COVID-19 crisis.

Key Points

Capital-to-risk Weighted Assets Ratio

|

Regional Rural Banks RRBs are financial institutions which ensure adequate credit for agriculture and other rural sectors. Regional Rural Banks were set up on the basis of the recommendations of the Narasimham Working Group (1975), and after the legislation of the Regional Rural Banks Act, 1976. The first Regional Rural Bank “Prathama Grameen Bank” was set up on 2nd October 1975. Stakeholders: The equity of a regional rural bank is held by the Central Government, concerned State Government and the Sponsor Bank in the proportion of 50:15:35 (PT SHOT). The RRBs combine the characteristics of a cooperative in terms of the familiarity of the rural problems and a commercial bank in terms of its professionalism and ability to mobilise financial resources. Each RRB operates within the local limits as notified by the Government. The main objectives of RRBs are

Reforms Recapitalization and amalgamation of RRBs RRBs became financially weak with many having high NPAs because of the difficult loans they are giving. A committee chaired by Dr. K.C. Chakrabarty reviewed the financial position of all RRBs in 2010 and recommended for recapitalization of 40 out of 82 RRBs. According to the Committee, the remaining RRBs are in a position to achieve the desired level of CRAR on their own. Accepting the recommendations of the committee, the central government along with other shareholders started to recapitalize eh RRBs by injecting funds into them. In the same manner the process of amalgamation continued. Amalgamation of RRBs were made in two phases and the number of RRBs were brought down during the first phase significantly. In the second phase of amalgamation and restructuring, which is ongoing from 2012, geographically extensive RRBs within a State under different sponsor banks are amalgamated to have just one RRB in medium-sized states and two or three RRBs in large states. Amalgamation of RRBs into sponsoring banks and their merger brought down the number from 196 in late 1990s to 56 by 2016. Most of the reform measures enabled the RRBs to make a smart recovery without being a burden and at the same time keeping their original risky mission of extending lending to the rural people. But still their NPAs remains high at around 6% (gross) and in the future also their activities need additional capital in the context of advanced capital requirements and regulatory standards. Hence, to enable them to acquire more capital the government has enacted RRB Amendment Act (2015). The amendment is aimed to help them to mobilize resource from financial markets. This Act let them to mobilize additional capital by keeping a combined government holding of at least 51%. RRBs Amendment Act 2015 The Regional Rural Banks (Amendment) Act, 2015, came into effect from 4th February 2016. The Act raises the amount of authorised capital to Rs 2,000 crore and states that it cannot be reduced below Rs One crore. The Act allows RRBs to raise capital from sources other than the existing shareholders -central and state governments, and sponsor banks. Here, the combined shareholding of the central government and the sponsor bank cannot be less than 51%. For the sponsoring banks, they can provide various initiating assistance to the RRBs beyond the initial five years (previously, the sponsoring bank’s responsibility will be over in five years). The Act states that the central government may by notification raise or reduce the limit of shareholding of the central government, state government or the sponsoring bank in the RRB. For this, the central government may consult the state government and the sponsor bank. |

![]() JAI HIND JAI BHARAT

JAI HIND JAI BHARAT

Source: TH/RRB

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

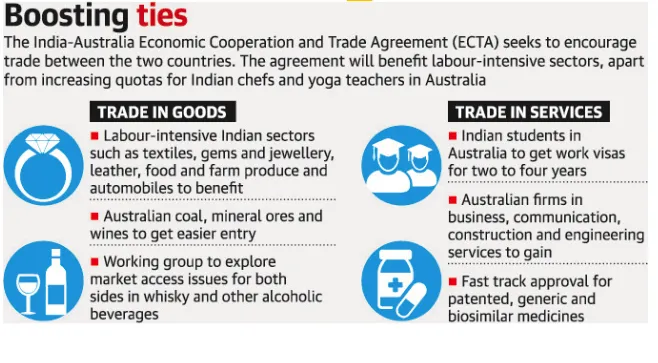

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

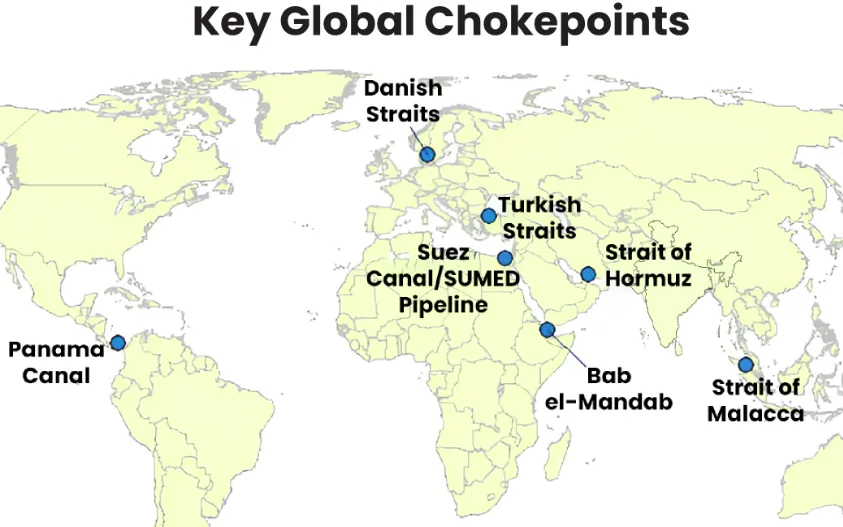

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment