Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

12 May, 2020

10 Min Read

Time for EU fiscal stimulus

Context

Germany’s highest court ruled last week that the European Central Bank (ECB) exceeded its mandate in pursuing Quantitative Easing (QE) to rescue the eurozone from the sovereign debt crisis.

The verdict is the culmination of fresh hearings that commenced in the country last year to apply the 2018 European Court of Justice decision to uphold the controversial programme.

Quantitative Easing

QE refers to the unconventional monetary tool of public sector asset purchases the ECB has deployed to stimulate economic demand and stoke inflation in the eurozone.

Germany Court

The court in Karlsruhe has asked the Frankfurt-based institution to justify its huge purchases of government bonds. Failure to furnish proof within three months that these purchases have not had a disproportionate impact on other economic policies risks jeopardising Berlin’s participation in QE, the court observed.

Claims and counterclaims

The ECB’s bond-buying under QE, of over €2.2 trillion since 2014, in order to raise eurozone inflation close to its 2% target, has long proved contentious in the eurozone’s affluent northern states.

Critics in Germany and the Netherlands argue that public debt purchases by the central banks of eurozone member states with ECB funding amounted to monetary financing of government spending by the ECB.

This has been barred under EU law, so as to insulate the institution from political pressures.

QE advocates refute the claim, insisting that the ECB was buying bonds from investors in secondary markets, not directly from governments.

They also point to the self-imposed cap on its holdings of up to one-third of the debt of any country and to acquire sovereign assets in proportion to the size of the economy, as measured by the share of ECB capital.

These constraints are intended as safeguards against potential defaults by member states.

Squabbling over rescue package

Germany’s monetary hawks moreover have their eyes set on the distorted real estate prices from the prolonged negative interest rates in the eurozone and the impact on lenders and pension funds to continue their assault on QE.

The Karlsruhe decision is believed to have no direct bearing on the ECB’s expansion of asset purchases by another €750 billion of bonds under the so-called pandemic emergency purchase programme until the year-end in response to COVID-19.

But the removal of the ceiling to acquire no more than one-third of a country’s debt could potentially expose the institution to fresh legal challenges.

The sustained attacks on the lender of last resort should serve as a wake-up call for eurozone leaders who are squabbling over the bloc’s rescue package for the post-pandemic recovery. Moves to mutualise the bloc’s debt acquire greater urgency than ever, as also calls for governments to infuse a bold fiscal stimulus.

The ECB has said it will continue its bond-buying programme, regardless of the implications arising from the Karlsruhe court ruling for the principle of central bank independence.

The decision also raises fundamental issues concerning the primacy of common EU laws at a juncture when the bloc is beset with eurosceptic and populist challenges from member states.

In the wake of the decision in Germany, the ECJ has emphasised its authority as the ultimate arbiter in all EU disputes.

Source: TH

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

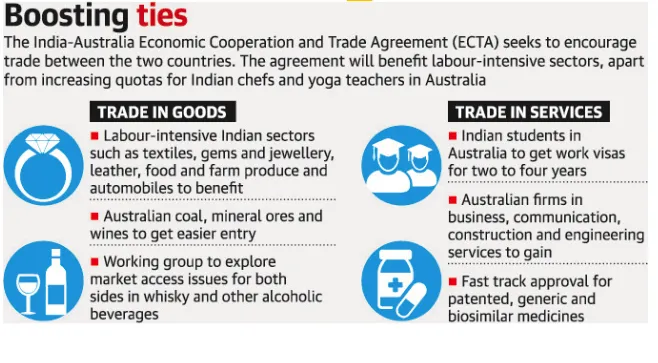

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

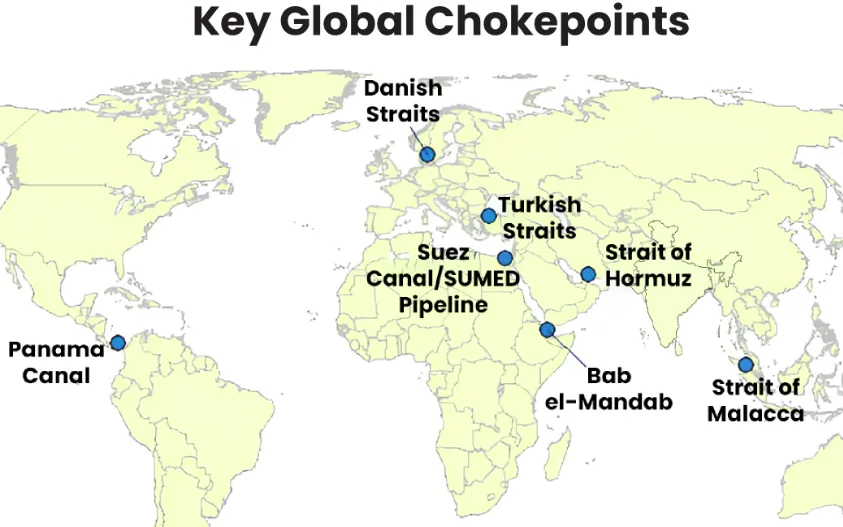

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment