Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

05 October, 2025

5 Min Read

India's ambitious plan to develop a fully indigenous solar manufacturing ecosystem by 2028 is an essential step towards achieving energy security, sustainability, and enhancing its position as a global leader in solar energy.

The solar manufacturing value chain involves multiple stages of production that convert raw materials into fully functional solar photovoltaic (PV) modules, which can then be installed for generating renewable energy. The value chain is typically divided into Upstream and Downstream segments:

Polysilicon: The process begins with metallurgical-grade silicon derived from quartz sand, which is refined into polysilicon.

Ingots: Polysilicon is melted and crystallized into large, cylindrical blocks, called ingots.

Wafers: Ingots are sliced into ultra-thin, disc-shaped sheets known as wafers, the building blocks of solar cells.

Solar Cells: Wafers are then treated with doping to create an electric field and receive a metallic coating for electricity conduction, becoming fully functional solar cells.

Module Manufacturing: Solar cells are interconnected, laminated between glass and polymer backsheets, and framed into a complete solar module.

System Installation & Integration: The modules are assembled into solar arrays, connected to inverters, mounting structures, and wiring, then installed on rooftops or solar farms.

India’s solar module capacity: 100 GW

Solar cell capacity: 27 GW

Ingot and wafer capacity: 2.2 GW

Despite India’s impressive solar module capacity, there is still a heavy reliance on imports, especially for solar cells, ingots, and wafers. This limits domestic manufacturing and poses a threat to energy security. However, the government is working towards resolving these gaps by boosting local production, particularly for polysilicon, a crucial component.

The challenges India faces in developing a domestic solar value chain are substantial and can be remembered using the mnemonic HURDLE:

H – High-Cost & Scale Issues: Indian-made solar components are initially expensive due to high manufacturing costs and lack of economies of scale.

U – Upstream Infrastructure Gaps: There are significant gaps in the polysilicon and wafer manufacturing sectors, which are capital-intensive and require advanced technologies.

R – RoW & Land Bottlenecks: Land acquisition and Right of Way (RoW) issues obstruct the development of large-scale solar projects.

D – Delayed Power Purchase Agreements (PPAs): Delays in PPAs by state governments and discoms create uncertainty, hurting project timelines and financial viability.

L – Lack of Experience: There is limited domestic experience in advanced solar manufacturing technologies.

E – Export/Import Dependence: Heavy reliance on imports, especially from China, weakens India’s energy independence and exposes the sector to external risks.

India has made notable progress in renewable energy, particularly solar power:

Renewable Energy Capacity: India has surpassed 251.5 GW of non-fossil energy capacity, achieving over half of its 2030 target of 500 GW.

PM Suryaghar Yojana: Over 20 lakh rooftop solar installations have been completed, with expectations to exceed 50 lakh soon.

PM-KUSUM Scheme: More than 1.6 million solar pumps have been installed, reducing diesel consumption by 1.3 billion litres annually and cutting CO2 emissions by 40 million tonnes.

India must take targeted steps to overcome challenges and develop a fully integrated solar manufacturing ecosystem. These steps can be remembered using the mnemonic SHINE:

S – Sustained Policy Support:

Expand the Approved List of Models and Manufacturers (ALMM) to include solar cells, wafers, and ingots.

Ensure stable production-linked incentives (PLI) and clear customs duties to protect domestic manufacturing.

Implement technology acquisition plans to enhance local expertise.

H – Harness Investment:

Attract investments for Greenfield manufacturing facilities.

Provide capital support to bridge gaps in upstream production.

Address land and RoW issues by creating a streamlined process for land acquisition.

I – Innovation & R&D:

Invest in next-generation technologies, such as Perovskite solar cells, to increase efficiency and reduce production costs.

Strengthen ancillary industries that supply raw materials and components.

N – Navigate Coordination:

Streamline state-level execution to ensure alignment with national policies.

Strengthen the financial stability of Discoms to enable smooth procurement of solar energy.

Align national schemes like PM Suryaghar Yojana and PM-KUSUM to drive demand for solar manufacturing.

E – Expand Demand:

Drive domestic demand for solar manufacturing through increased policy incentives and deployment programs.

Encourage widespread adoption of solar through subsidies, net metering, and tax breaks.

To achieve net-zero emissions by 2070 and meet its target of 1,800 GW renewable energy capacity by 2047, India must develop a robust, indigenous solar manufacturing ecosystem. This requires a comprehensive, integrated approach to overcome challenges like high costs, infrastructure gaps, and dependence on imports. By focusing on policy support, investment, innovation, and coordinated execution, India can strengthen its solar manufacturing sector, improve energy security, and bolster its position as a global leader in clean energy.

Source: PIB

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

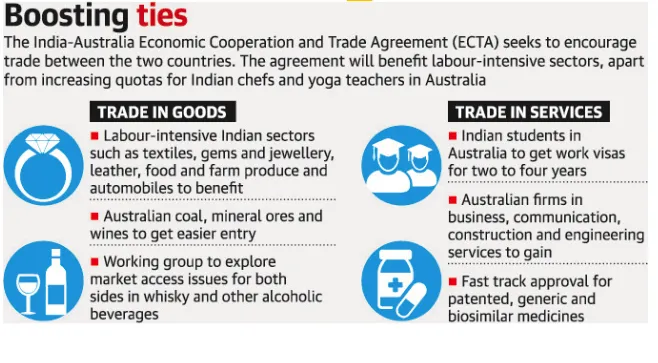

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

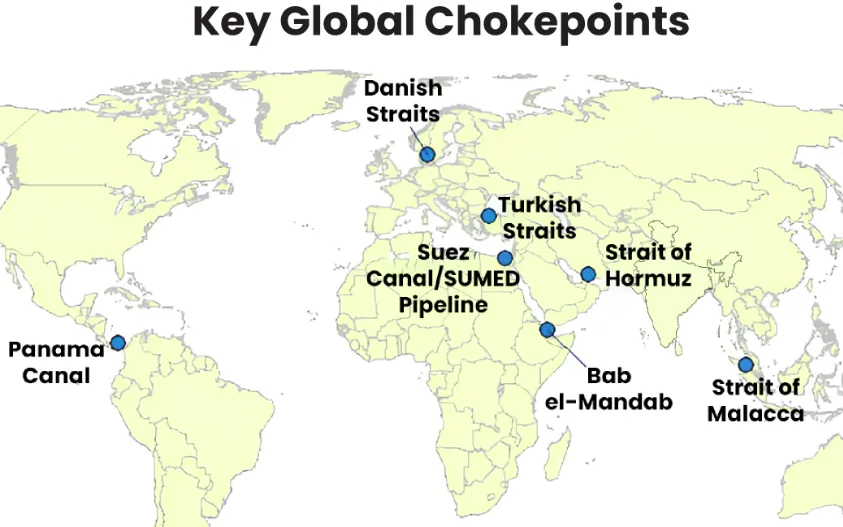

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment