Online Learning Portal

Online Learning Portal

Hybrid Classes

We provide offline, online and recorded lectures in the same amount.

Personalised Mentoring

Every aspirant is unique and the mentoring is customised according to the strengths and weaknesses of the aspirant

Topicwise Mindmaps

In every Lecture. Director Sir will provide conceptual understanding with around 800 Mindmaps.

Quality Content

We provide you the best and Comprehensive content which comes directly or indirectly in UPSC Exam.

DAILY NEWS ANALYSIS

02 December, 2019

Min Read

Syllabus subtopic: Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment.

News: The reserve Bank of India (RBI) is expected to cut rates further by 25 basis points, after the 135-basis-point cut in its policy rate, at this week’s monetary policy review in the backdrop of the deepening slowdown and projections of a sub-5 per cent growth this fiscal year.

Prelims and Mains focus: about the recent credit slowdown and the efforts to check it, performance of various sectors, about credit offtake

Context

The central bank, which cut the real GDP growth for 2019-20 to 6.1 per cent in October from 6.9 per cent in forecast in August, reflecting the ongoing slowdown in the economy, is set to slash the growth estimate further. The sharp fall in GDP growth to 4.5 per cent in the September quarter from 5 per cent previously provides enough reason for the RBI to cut the rate, analysts said.

Though the RBI has cut rates by 135 bps in 2019, banks have passed on only 29 per cent to customers and growth in credit offtake has declined, indicating that the RBI’s strategy to push up demand has not worked so far. Credit offtake increased by a meagre 0.8 per cent (Rs 75,794 crore) in January-November 8 of FY20, compared to 5.6 per cent (Rs 4.86 lakh crore) in the same period of last year. In the current fiscal year so far, credit growth continued to decline to 8.1 per cent as compared to last year growth of 14.9 per cent, on high base effect.

What does the analysis say?

A deeper analysis of the data indicates that though till the end of August 2019, credit growth was declining, the trend has reversed since September and credit growth has jumped by Rs 1.67 lakh crore,

With the liquidity crunch and defaults rocking the financial sector, NBFC sanctions fell 34 per cent to Rs 1,95,205 crore in the September quarter from Rs 2,93,957 crore in the same period of last year, according to Finance Industry Development Council (FIDC).

Banks, on the other hand, have turned very choosy about credit sanctioning and disbursals, fearing fresh loan slippages.

The sectoral data for October 2019, which accounts for about 85 per cent of the bank credit deployed by 39 banks, indicates that credit to industry and services has declined incrementally by Rs 1.62 lakh crore, while credit to agri and allied and personal loans increased by Rs 1.92 lakh crore. Within industry, credit to paper and paper products, all engineering and infrastructure has increased in October 2019 and credit to all other sectors has declined.

Manufacturing growth contracted, while both private consumption and investment stayed weak. Given this, and with the just-released index of eight core industries falling 5.8 per cent in October, bottoming-out of growth could be further down the road and recovery is unlikely to be V-shaped as consumer demand, credit supply and risk appetite remains lacklustre. This and the falling core-CPI (consumer price inflation) should allow the RBI focus more on growth.

All the indicators ranging from IIP (index for industrial production), electricity consumption to core inflation rate were pointing towards the fact that the economy has not entered the revival path.

The slowdown in consumption is indeed worrying, as its revival is important for investment to pick up.

What is PFCE?

The Private Final Consumption Expenditure (PFCE) declined to 5 per cent compared to 9.7 per cent. With growth slipping to 4.5 per cent, it is expected that RBI will go for the next round of rate cut in December.

PFCE is defined as the expenditure incurred on final consumption of goods and services by the resident households and non-profit institutions serving households.

The tepid domestic growth has been led by weak investment activity, moderate consumption growth and slow global growth environment. While further policy support can be expected from both the government and the RBI, the recovery is expected to be more gradual than a V shaped sharp recovery.

About credit offtake

Simply put when Trade and Industry and other sectors start using Bank Funds either from the existing limits sanctioned to them or by availing fresh credit limits , Credit portfolio of the Banks increases which in Banking parlance is called Credit Off take and that results in:

Note: to know more about the efforts of the govt. to boost economic growth click on the link below

Source: Indian Express

A year after tensions arising from Operation Sindoor, India and Azerbaijan have taken steps to restore and normalise bilateral relations. The 6th round of Foreign Office Consultations, held in Baku, marked the first such engagement since 2022, signaling renewed diplomatic momentum. Recent Diplomatic Engagement During the consultations, bo

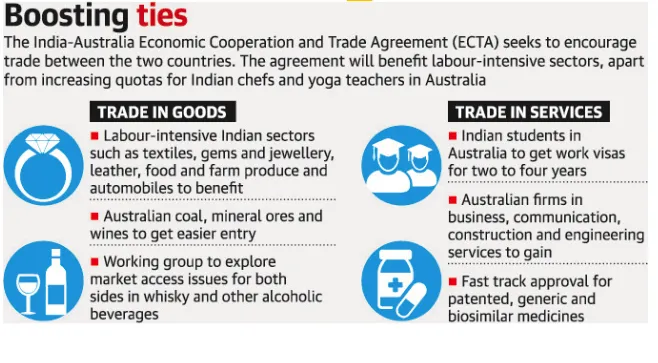

The India–Australia Economic Cooperation and Trade Agreement has completed four years since its signing. Both countries now aim to build on this progress through strengthened collaboration and ambitious targets, including reaching AUD 100 billion in bilateral trade by 2030. What is the India–Australia Economic Cooperation and Tra

A recent report by the Association for Democratic Reforms (ADR) analyses donations of ?20,000 or more declared to the Election Commission of India (ECI) by national political parties for FY 2024–25, highlighting transparency and accountability in political financing. Key Findings Massive Funding Surge Total donations to nationa

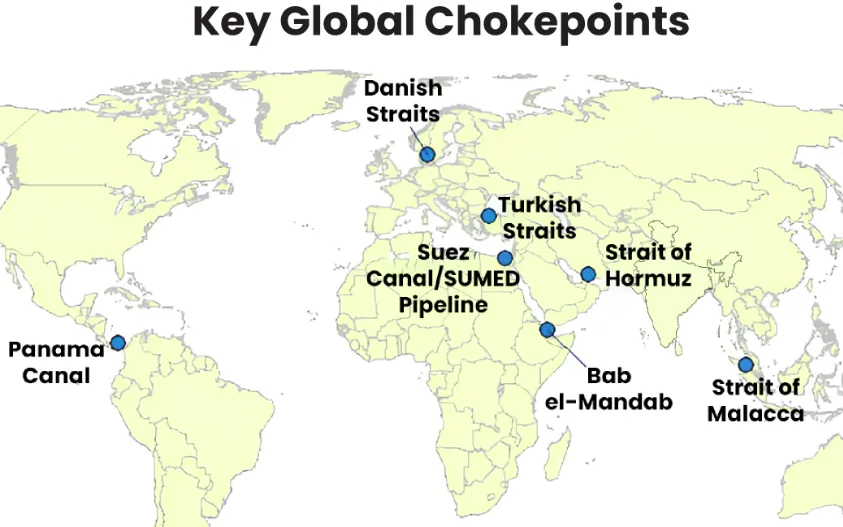

Maritime chokepoints are narrow channels along global shipping routes where maritime traffic is concentrated. These points are geopolitically and economically critical, as they handle a large proportion of global trade, especially energy shipments. Current Relevance Over two-thirds of seaborne energy trade passes through a handful o

Following the launch of Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the geopolitical landscape has shifted fundamentally with the confirmed death of Iran’s Supreme Leader, Ayatollah Ali Khamenei.Iran retaliated through Operation True Promise 4, launching missile attacks against Israel and nearby Gulf states. The escala

Our Popular Courses

Module wise Prelims Batches

Mains Batches

Test Series

My Notes

My Notes

Geography And Environment

Geography And Environment